How to Upload Letter to Credit Bureau

This blog post is for the people who cannot afford my paid credit repair services and don't mind going through the problem of repairing credit themselves.

For them, I've distilled my 15 years of experience of fixing credit scores into an advanced method credit agency dispute letter of the alphabet with specific instructions on how to utilize it.

Because let'south face it, trying to remove a 30-day tardily payment or repair your credit yourself can go overwhelming and confusing:

— It'south difficult to figure out how to dispute correctly

— Credit Bureaus may disregard your disputes

— Creditors keep on verifying your challenges

And if you've hired a credit repair visitor or so-called "police force firm" like Lexington, chances are:

— you've wasted $1000+ without results in upfront fees

— they put in ineffective credit bureau disputes and goodwill requests

— you find yourself at the same place where you started

Are you lot still committed to learning how to do this? Proficient. It will take attention to detail, but if you have the fourth dimension to learn, this will pay off.

Here'south what you need to know:The Fair Credit Reporting Act'due south (FCRA) Department 611 allows for consumers to claiming questionable items on their credit reports.

This includes tardily payments accuse-offs, collections, revenue enhancement liens, bankruptcies, judgments, foreclosures, or any personal identification information.

What this means is, virtually any "questionable" negative data the credit bureaus have for you can exist disputed and their deletion may upshot in a credit score increment.

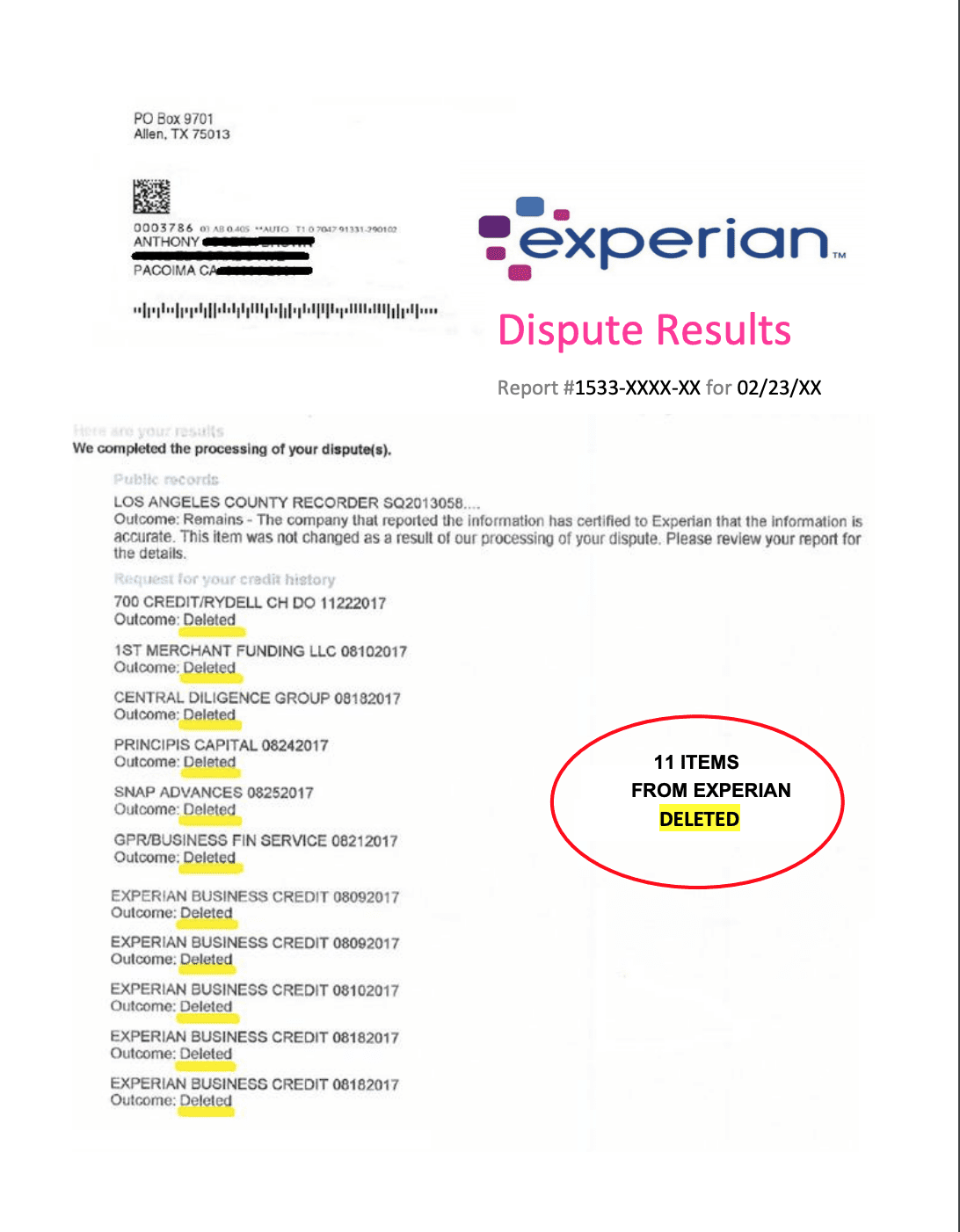

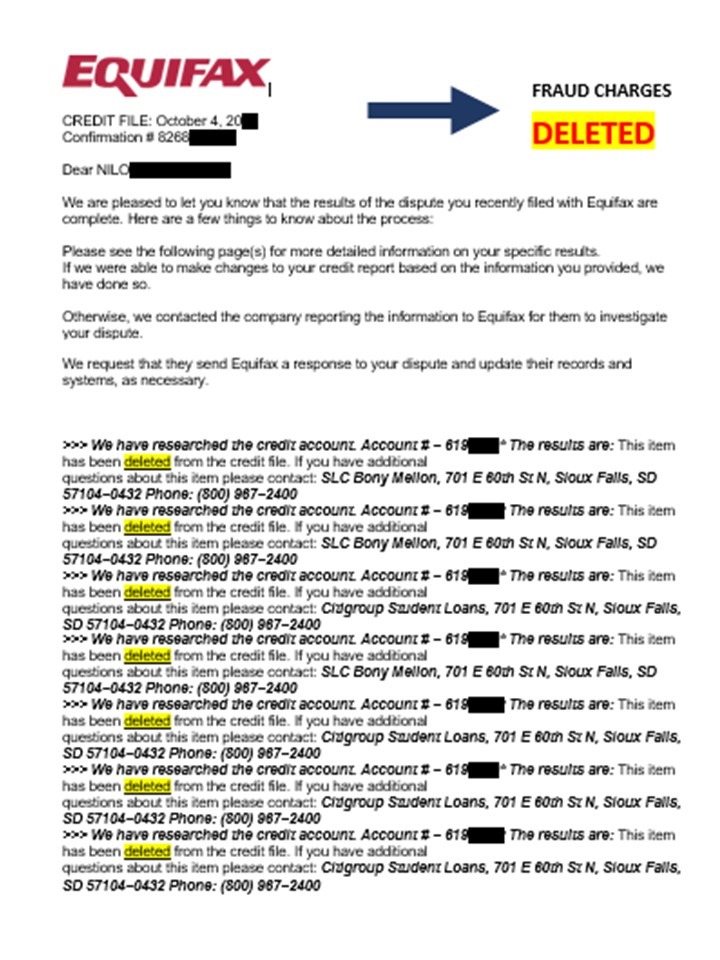

Proof this letter works, Check out these results I've got for my clients!

These are actual confirmation letters from credit bureaus confirming removal of accounts:

Want more proof?

Scroll downwardly to the bottom of the page and check out my Yelp reviews.

Now, permit'south get-go with the basics.

How to dispute accounts with credit bureaus: Phone, Postal service, Online or Fax?

About consumers dispute accounts by telephone or online.

This is a huge error!

Experian, Equifax, and Transunion allow you lot to pull a credit report straight from their websites, or from annualcreditreport.com, or through sites like CreditKarma.

Those reports will provide y'all with a link to dispute online and a telephone number for the credit bureau's customer service dispute heart.

Phone and online disputes, although peradventure the simplest ways to dispute. Any serious credit repair expert will tell you never to use this method.

Why? Consumers are at a disadvantage every time they do this.

Firstly, the credit bureaus make consumers agree to innocuous-sounding waivers, which in fact make clients surrender their rights to re-investigation.

Second, without a proper paper trail, the credit bureaus practice non have to fear the threat of lawsuits. And then the credit bureaus tin have online and phone disputes less seriously.

This means less thoroughly investigated disputes that lead to items not being deleted from the credit report.

So using an actual credit dispute letter and mailing or faxing will serve you much better.

Watch this video to understand your state and federal rights, and how to utilize them to protect yourself and repair your credit:

Common mistakes to avoid with credit dispute letter

So over the years, I've seen clients of mine brand errors that end upward hurting their chances for deletion.

Here are means to avoid these mistakes:

A) Yous shouldn't threaten legal action of any kind unless you lot have reason to exercise and then.

B) Do not dispute any positive items on your credit report, once removed they cannot be re-inserted.

C) Do not dispute any inquiries linked to accounts you've legitimately opened, your enquiry dispute will be forwarded to the creditor, who may close the account fearing fraud.

D) Make certain to include entire account numbers if the aforementioned creditor is reporting multiple accounts. You do not want the wrong account disputed and deleted.

What accounts you should never challenge with credit bureaus

I absolutely cannot stress this enough;When trying to repair your credit, DO NOT dispute whatsoever legitimate debts that fell behind recently, which you cannot afford to pay off.

Here'south why – Creditors can legally sue consumers within the statute of limitations they are allowed past the land the debtor resides in.

So, check the statute of limitation for debts in your states earlier disputing any large unpaid accounts.

For instance in California, the statute of limitations for debts is 4 years.

Hither's what this means:

If you live in California, creditors can sue yous for up to four years from the fourth dimension you defaulted on a debt

Disputing accounts that lie within the statute of limitations may incite the creditor to take legal activeness against y'all.

This, however, does not pertain to items that are resulting from identity theft.

Volume YOUR FREE CONSULTATION

What accounts you lot can remove with the credit report dispute letter

You can dispute the following items:

Credit account-related Disputes: Charge-offs, late payments, missed payments, collections, repossessions, student loans, installment loans, car loans, mortgage foreclosures. Virtually whatever account that is reporting on your credit file.

Public records: These include, IRS tax liens, state taxation liens, judgments, and bankruptcies.

Credit Inquiries: Requests for your personal credit report, aka credit inquiries, are recorded past the credit bureaus and kept on record for 2 years. You lot can dispute credit inquiries that are questionable and improve your score past getting them deleted.

Personal data: Y'all tin can dispute to get removed or accept the bureaus update all your personal information including your name, current address and previous addresses, your phone number, your employment data, your date of birth, and SSN#.

How to dispute recent belatedly payments and recent collections

Something you must know – Any valid or contempo collection, or recent late payments, cannot be removed from your credit report with a credit bureau dispute alphabetic character.

How to remove these:

Recent late payments: For recent tardily payments inside the last two years or on open up accounts, the just way to get these expunged is by utilizing the direct creditor dispute method. For older belatedly payments, the credit agency dispute alphabetic character would work.

Recent collection accounts: For recent drove accounts, which fell behind within the last 4 years that are valid, the virtually effective way to become these expunged is to use the pay for delete method, where yous offer to settle the account in exchange for deletion from your credit report.

Older collection accounts: Or for re-aged drove accounts, you'll need a debt validation letter, where you challenge the debt with the debt collector first.

After the collection company receives your letter, just so should you ship out a credit bureau dispute letter. This way the collector is being asked for verifications on ii fronts, by you directly and from the credit bureaus likewise.

The credit bureau dispute letter

Full Name

Mailing Accost:

Appointment of Nativity

{If Sending to Experian: P.O. Box 4500, Allen, TX 75013}

{If Sending to Equifax: P.O. Box 740256, Atlanta, GA 30374-0256}

{If Sending to Transunion: Consumer Disputes, P.O. Box 2000, Chester, PA 19016}

{Date}

RE: Investigation Request to Delete Credit Inquires

To whom it may concern,

In accordance with the Fair Credit Reporting Act Section 611 (15 U.Due south.C. § 1681I), I am practicing my right to challenge questionable data that I have found on my personal credit report. I do not recognize the information listed below and request that y'all investigate the source of these accounts and define that the creditor had a permissible purpose, and is able to verify my complete file information including total name, address, date of birth and SSN#.

Incorrect Business relationship Information

The accounts below are reporting incorrectly please investigate these:

ane. {Creditor Name} {ac#} {Reason for Dispute}

2. {Creditor Name} {air conditioning#} {Reason for Dispute}

3. {Creditor Name} {air-conditioning#} {Reason for Dispute}

Incorrect CREDIT INQUIRIES

I am disputing the post-obit inquiries which I did not authorize:

1. {Creditor Name} {inquiry date}

2. {Creditor Name} {inquiry date}

REMOVE INCORRECT PERSONAL INFORMATION

I am disputing the following personal information that is showing for me which is incorrect:

one. Incorrect SSN {xxx-xx-20 xx }

2. Incorrect Accost { insert address}

three. Incorrect Proper noun Variations { Insert proper noun}

UPDATE PERSONAL INFORMATION

Also delight update the following information which I saw your credit agency to be missing or incomplete:

1. Personal current accost {insert correct address}

2. My proper full { insert your correct total name, if the bureau has listed it incorrectly}

iii. My date of birth { insert engagement of birth, if bureau has information technology listed incorrectly}

4. My current employment info { insert employer name, address and your position, if the agency is missing this info}

I am allowing you lot 30 days to consummate this investigation after which I authorize you lot to mail me my updated credit reports along with the investigation results

Truly,

{Name}

{Signature}

How to fill out the credit dispute alphabetic character

STEP i: Place yourself

Fill in your personal identification information, current address, appointment of birth, and SSN.

STEP 2: Choose items to dispute

List the erroneous personal identification information you are disputing along with a list of the questionable accounts and inquiries.

For each account, list the creditor proper name and the account #, along with the reason for your dispute.

Pace iii: Cull a reason for disputing each item

The Account does not vest to me. The account payment history is incorrect.

The account is besides one-time to exist on the credit written report. The business relationship was paid prior to collection. Incorrect amount. Incorrect final payment appointment. Incorrect Condition. The account belongs to someone else with a similar proper name.

Virtually whatsoever questionable aspect of an account can exist deleted

Footstep 4: What to enclose with the Credit Agency Dispute Letter

–Photo ID: This could be any land or government-issued identification

–Proof of Residency: This could be a contempo utility pecker, or bank statement, mortgage statement, or a copy of your habitation rental understanding. Information technology should show your name and electric current mailing address.

— Proof of SSN#: This could be whatsoever land or government document showing your SSN#. Or a page from your revenue enhancement return, W-2, paystub, or 1099, etc.

Whatsoever Supporting Documentation: This could include anything that could support your dispute claim, like a letter of deletion from the creditor.

STEP 5: How to Mail service:

These messages should be mailed out via certified mail and e'er relieve the greenish receipt from your records.

Stride 6: Await for 30 Days for the Dispute Completion:

Inside thirty days after receipt of the letters past the credit bureaus, you should receive the investigation results from them.

SIMILAR READ: How to Remove Charge-Offs from a Credit Report

The results volition show what accounts were disputed and whether they were deleted, updated with new information, or remain unchanged.

Book YOUR Gratis CONSULTATION

What to do if the credit bureaus practise not correct your credit report

Sometimes the bureaus won't transport you the investigation results, every bit they may deem your identification data incomplete.

Regardless, they are required to investigate the items you requested.

And then, here's what y'all practise:

Pull your updated credit report afterward well-nigh 35 days from the fourth dimension you mailed out the dispute messages.

And then check on each bureau if there take been any deletions or any accounts showing they are "under re-investigation."

These two indicators should let yous know if the bureaus actually investigated your claim or not.

If you observe no such indicators, refer back to your certified mail tracking information and ostend the bureaus received the letters.

If the messages were received, then you tin can move to lodge complaints against the bureaus, every bit discussed below.

>How to file regulatory complaints against the bureaus and creditors

In the event that the bureaus practise not investigate or right your credit report,

Then you accept more extreme measures…

Y'all guild a regulatory complaint with the Consumer Financial Protection Bureau (CFPB) at www.consumerfinance.gov.

What's bang-up about the CFPB is, you can also society complaints against creditors and drove companies here.

The CFPB frontwards these complaints to the party you lodge a complaint, who must answer back to the CFPB within thirty days with a resolution.

They likewise collects data on the number of complaints filed confronting each establishment and may take regulatory action against them if they detect a pattern of violations.

BOOK YOUR Gratuitous CONSULTATION

Using the Section 604 dispute letter of the alphabet/ Method of Verification Letter

At present if the CFPB compliant doesn't do the trick

Hither'due south what you do and so:

You exercise your right under the FCRA Section 609 and Section 604 to request a method of verification.

Through another important tool known as the department 609 dispute letter or section 604 dispute letter, both dispute letters are like.

This is how it works – yous're asking the creditors to provide you with details pertaining to how and with whom they verified the information yous disputed.

The Sample Method of Verification letter

All you'll need to practice is simply arrange the first credit bureau dispute letter yous sent them and put in the following text:

I sent your company my dispute on {Date}, which y'all received and investigated on. I have reason to believe that you conducted a reasonable investigation. therefore, I am invoking the Fair Credit Reporting Act Section 611 to ask that you lot provide me with the following information:

1. The date you contacted the creditor

2. The contact information for the creditor

3. The proper name of the person who verified the item to you lot

4. The method of communication yous used to verify this information

5. Did the creditor provide yous with my SSN, address, and Date of Nascence?

Volume YOUR Free CONSULTATION

rutledgethowithid.blogspot.com

Source: https://www.imaxcredit.com/credit-dispute-letters-credit-bureau/

0 Response to "How to Upload Letter to Credit Bureau"

ارسال یک نظر